12 Graphs That Show Just How Early The Cryptocurrency Market Is (May 2018)

This post was originally written on April 11th, 2018 on Medium.

From the time the first website was published in 1991 until today, the internet has profoundly reshaped humanity.

Comparisons between cryptocurrencies and the growth of the internet are invariably drawn (including cryptocurrencies’ netscape moment); however, I wanted to test this comparison and see exactly how far along we are.

In this post, I’ll also be exploring the growth of the cryptocurrency market & the early growth of the internet, to see what takeaways we can uncover.

What makes this comparison tough

It’s impossible to know exactly how many people use cryptocurrency and how often because:

For people who self custodial their cryptocurrencies — people can have multiple wallets for different cryptocurrencies.

For people who store their cryptocurrencies on exchanges — 1 wallet address does not equate to 1 user on the exchange. It’s also typical for exchanges to create a wallet address for each transaction.

Thus, the only way to get an understanding of the number of users for cryptocurrencies is through approximations.

Measuring cryptocurrency user growth

I tried to approximate cryptocurrency user growth in a few ways:

Bitcoin & Ethereum wallet growth

Bitcoin & Ethereum active addresses growth (proxy for DAU)

User growth of crypto-fiat and crypto-crypto exchanges

Total cryptocurrency trading volume over time

There are ~24M bitcoin wallet addresses in total. This doesn’t mean there are 24M Bitcoin users because one person can have more than 1 wallet address and it is recommended to generate a new bitcoin address for each transaction sent.

I would consider 24M the upper bound number on the number of bitcoin users worldwide. (from a pure non-custodial perspective).

In addition to looking at the number of wallets, we can look at the number of active addresses per day. To smooth out this chart, I took a median value of active addresses by month, and plotted it on a log scale:

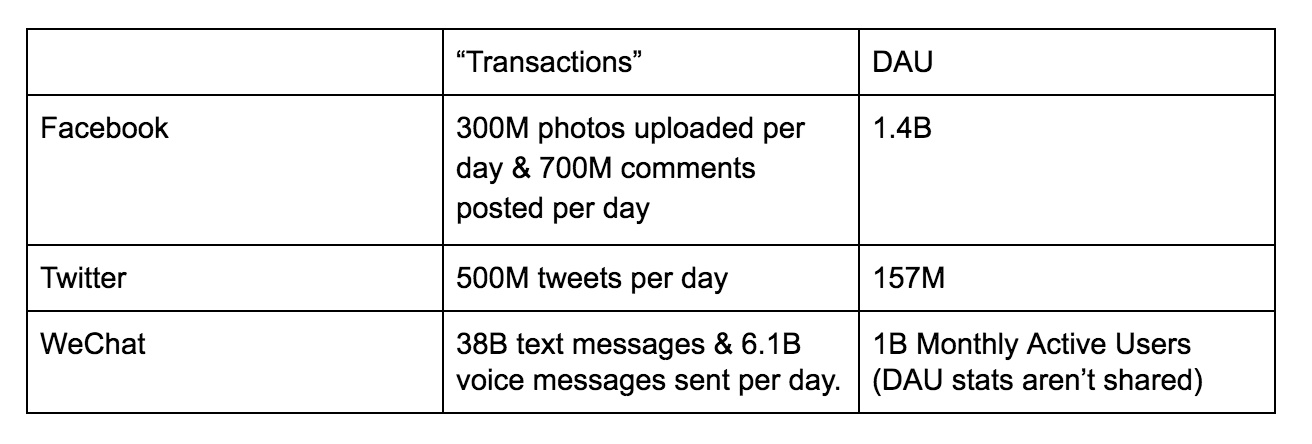

The highest amount of active addresses we’ve seen per day was ~1.1M addresses — this is an approximation of daily active users (DAU) within the bitcoin network. However, if the main point of Bitcoin is viewed as purely a store of value, then you would assume a much lower DAU vs. any traditional mobile application or website.

We can also do the same analysis for Ethereum, here is the Ethereum address growth and active addresses per day (in log scale):

In total, there are 31M Ethereum addresses with peak daily active addresses on the Ethereum network reaching 1.1M.

Ethereum is a bit different than bitcoin because smart contracts have their own addresses and usage on Ethereum should naturally be higher since Ethereum is designed as a smart contract platform, not as a pure store of value.

Users of bitcoin and users of ethereum are not mutually exclusive as well, I would assume a high degree of correlation between the two cryptocurrencies.

Another method to approximate the user growth of cryptocurrencies is to instead look at the exchanges themselves — both fiat-crypto and crypto-crypto exchanges.

Only a handful of crypto exchanges have published their total user stats & user growth statistics. Here is what I could find:

If we take all of the exchanges trading with fees, here is a breakdown of the market share by all of the crypto exchanges (including fiat and crypto-crypto):

Furthermore, if we take all of the exchanges where we know the user counts and trading volume, we can come up with an estimated trading volume per user. Through this number, we can forecast across all trading volume what theestimated users of cryptocurrencies as a whole are: 20.2M users.

I would consider this the lower bound on the number of cryptocurrency users based on the number of people who are trading & purchasing cryptocurrencies across all of the various exchanges.

Furthermore, we can also look at the overall trading volume of all cryptocurrencies over time to see how trading volume have been trending from 2014–18. The chart below is also in log scale and the values have been averaged out per month to get a better sense of the overall trend line.

While all of these measurements are not exact counts of users, I would approximate the total users of cryptocurrencies to be between 20M-30M people in total worldwide.

Comparing the growth of cryptocurrency users to the growth of internet users

Now that we have an estimate on the total number of cryptocurrency users worldwide, we can look at the growth of the internet and estimate how early we are in this trajectory.

Here is the growth of internet users:

If we zoom into 1990–1995 for the internet compared to 2013–2018 in cryptocurrencies:

You can see we’re actually tracking quite closely with the early days of the internet. If you think cryptocurrencies is going to follow a similar trajectory as the internet, we look like we’re in about year 1994 compared to the internet.

We can also do a similar analysis comparing the number of websites in the early internet to the number of crypto projects in the space — for this I’m taking the total number of cryptocurrencies & tokens + all of the DApps.

Here is the growth trajectory of the number of websites:

If we zoom into 1991–1995 in the growth of websites compared to 2014–17 in the growth of crypto assets (tokens which received funding +DApps):

We are at year 1994 on this comparison as well. For one last comparison we can look at the total number of internet companies which received funding from 2014 to 2017 compared to the number of internet startups that got funding from 1991 to 1995.

*Funding amounts are adjusted for inflation and only account for internet/software company financings.

My takeaways:

Even though we’ve seen a huge increase for number of users of cryptocurrencies, tokens, and DApps — we are still in year 1994 if we compare the trajectory to the growth of the internet.

However, depending on your long-term view of the core-use cases of blockchains & cryptocurrencies, the analogy is either an apt analogy or a pointless endeavor:

If you view the core use-cases of cryptocurrencies as a new asset class then I wouldn’t necessarily expect cryptocurrencies to follow the same trajectory as the internet — both in terms of user growth & growth of assets (equivalent to websites on the internet).

If you view the core use-cases of cryptocurrencies as an application platform for decentralized applications (DApps) — or better known as the decentralized internet — then the growth of users & DApps would be comparable to the growth of internet users & website growth.

My biggest criticism towards the DApp future is we haven’t seen DApp usage keep pace with the number of DApps being created. The current core use cases of cryptocurrencies are speculation, store of value, assets, payments, etc.

Looking at the data we can see the use case of cryptocurrencies as an asset class has considerably more proof points and measurable user adoption.However, the future of decentralized applications, while interesting to track, is still too early to measure.

A big thank you to Ricky Tan for contributing data from TokenData & feedback for this post & thanks to Noah Jessop and Kim McCann for providing feedback on this post.